Lifestyle

Consumer Credit Act: What Buy Now Pay Later Users Need to Know

Learn how Malaysia's Consumer Credit Act 2025 protects you from Buy Now Pay Later (BNPL) traps with transparency, fair terms, and debt help options.

Learn how Malaysia's Consumer Credit Act 2025 protects you from Buy Now Pay Later (BNPL) traps with transparency, fair terms, and debt help options.

TL; DR

If you have ever bought the latest iPhone or sneakers using a Buy Now Pay Later (BNPL) payment method, you are not alone.

Many young Malaysians are swiping left on old-school credit cards and choosing flexible BNPL options instead. It feels easy, interest-free (at least upfront), and friendlier on your cash flow.

But here is the catch: many BNPL users do not realise that those “small” monthly payments add up, and if you miss even one, fees stack up fast. The government has noticed this trend, and with bankruptcy rates among young adults in Malaysia on the rise, Parliament has stepped in with the Consumer Credit Act 2025 (RUU Kredit Pengguna 2025).

This new law is here to make BNPL safer, clearer, and less likely to trap you in debt. Let’s break it down in simple terms.

BNPL is basically an instalment plan without a credit card. Instead of paying RM2,400 for a new phone upfront, you split it into smaller monthly payments, often 3, 6, or 12 months.

It is tempting because:

But BNPL is still a loan, not “free money.” If you miss payments, late fees and penalties will be charged, and multiple BNPLs running at once can quietly eat up your paycheck.

The Consumer Credit Act (CCA) 2025 is a new law recently passed by the Dewan Rakyat to regulate BNPL providers, moneylenders, and other consumer credit players.

Why now? Because many Malaysians especially those in their 20s and 30s are using BNPL without realising the long-term financial risks.

The Act makes sure companies are licensed, transparent, and accountable so consumers are not left in the dark.

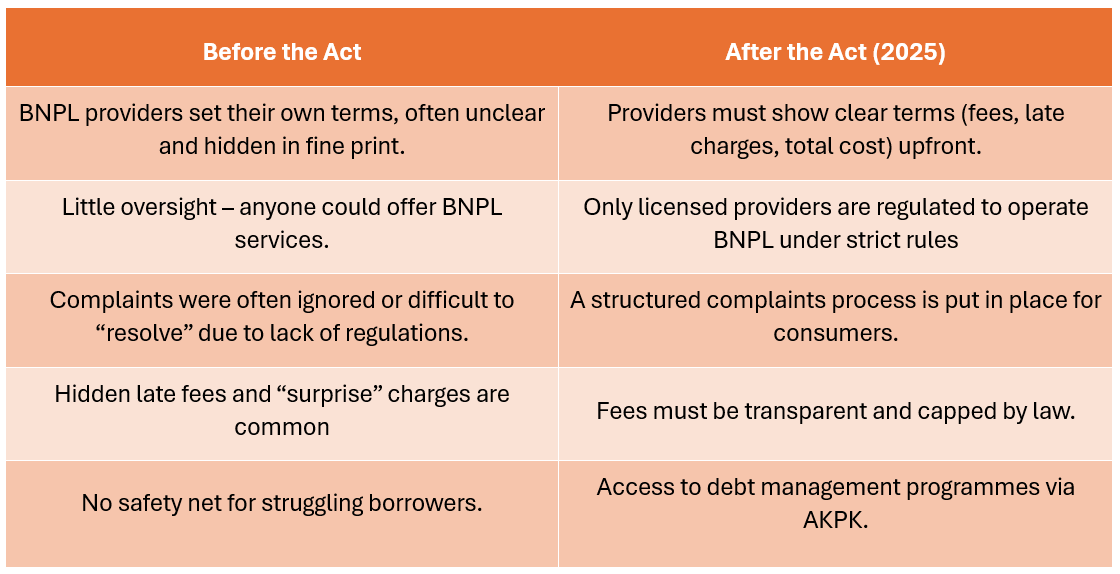

Here is what changes for BNPL users under the new law:

Think of it like a seatbelt for your finances. You can still drive fast and within the speed limit, but with more protection if something goes wrong.

Because this law is designed with you in mind. Statistics show young adults are the largest BNPL users in Malaysia, and many are also the most vulnerable to debt traps. With rising living costs, it is easy to blur the line between needs and wants.

The Consumer Credit Act does not stop you from using BNPL, but it makes sure:

Let’s say you want the latest iPhone, priced at RM4,799. With BNPL, you split it into 12 monthly payments of RM400.

Before the Act: The app could apply late fees or administrative charges without clearly notifying users, especially if a payment was missed.

After the Act: You will see the true cost upfront including fees. Late charges are capped, and if you are struggling, you can seek help from AKPK to restructure payments.

It is still your choice to buy but now, you get to decide with eyes wide open.

If your BNPL or other debts are overwhelming, you can reach out to Agensi Kaunseling dan Pengurusan Kredit (AKPK). They offer free financial counselling and can negotiate with lenders on your behalf to set up a realistic repayment plan.

Signing up is simple: visit their website, call their hotline, or walk into an AKPK branch. Many young Malaysians have already taken this step and come out stronger.

The new law helps, but real financial freedom comes from your own habits. Here are three golden rules to live by:

The Consumer Credit Act 2025 is here to here to ensure greater transparency, fairness, and protection for consumers.

Use BNPL if it fits your lifestyle, but always remember to spend smart, know your limits, and protect your future self. Because at the end of the day, the latest gadget is not worth a lifetime of debt.

Click here for PIDM’s TIPS Brochure.